Hunger Games

Today, Fedex announced their same-day delivery robot which signals another major player throwing their hat into the 'autonomous delivery bot' ring - following in the footsteps of Amazon Scout, Softbank-backed Nuro, Marble, Kiwi, and others.

Recently, I have been researching and thinking about this space where it seems like technological differentiation is minimal. It is essentially an AI driven 'service' where other than load-bearing specifications and radius of service, the bots can only be differentiated on their looks.

According to this McKinsey Report (which every single robodelivery company cites), autonomous delivery robots/vehicles (what do we classify them as?) will be responsible for 80% of all last mile deliveries. This is mostly driven by this basic business objective - reducing cost.

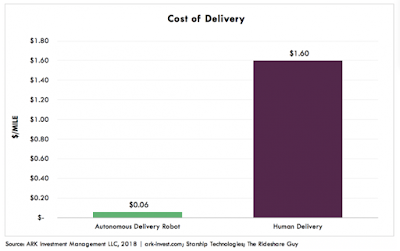

Last mile delivery is the biggest cost driver in the delivery landscape. Because of economies of scale, it is cheaper to ship bulk items from a centralized location/warehouse to local delivery centers than it is to ship individual items from your local delivery center to your house. More specifically, the cost per delivery per last mile for human delivery is $1.60 while a robodelivery agent gets the job done for only $0.06.

Now let's do this math at scale. If Amazon delivers 5 billion Prime packages per year, they incur $8 billion in last mile delivery charges if a human delivers it. In comparison, it only costs $300 million using autonomous delivery robots. It's a no-brainer for Amazon. This is the reason Amazon acquired Dispatch, Softbank invested almost $1 billion into Nuro, and JD launched their own driverless delivery robot.

Lots of players - how to win?

Currently, there are over 15 venture-backed (or corporate-developed) companies operating in this space. As I mentioned, form factor is the biggest difference among these companies. This means the secret to winning in this industry is a massive partnership landgrab. The larger the network of retailers serviced by these delivery companies, the greater their odds of success. Unfortunately, as Uber/Lyft demonstrated, in the absence of technological differentiation, when switching costs are extremely low, brand loyalty is simply distributed among the top 3 most convenient players. In food - everyone uses a combo of Uber Eats, Postmates, Grubhub, and Doordash. In ride-sharing, Uber and Lyft. I am sure consumers will settle on the top two or three apps that have the most retailer delivery partnerships.

There are a lot of players in the industry and I expect a lot of consolidation in 2019 and 2020. Amazon and JD have made their move by launching their own autonomous delivery robots. Doordash has tried partnerships with several autonomous robodelivery companies and it makes sense for them to consider acquiring one because they already have a network of restaurants. Similarly, chains like Dominos and Pizza Hut also have the network to succeed in this market. Let the acquisition and partnership hunger games begin!

Well no matter who wins this bloodbath, at the very least, you don't have to make small talk with your delivery robots...!